Abstract

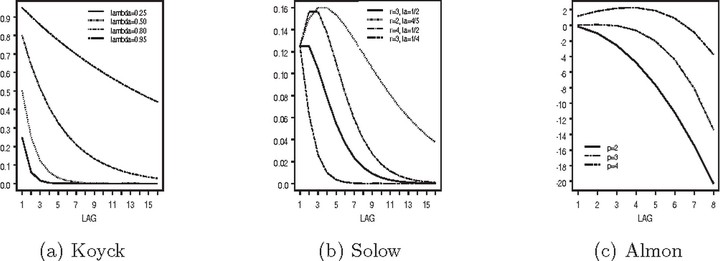

This paper aims to show to practitioners how flexible and straightforward the implementation of the Bayesian paradigm can be for distributed lag models within the Bayesian dynamic linear model framework. Distributed lag models are of importance when it is believed that a covariate at time t, say Xt, causes an impact on the mean value of the response variable, Yt. Moreover, it is believed that the effect of X on Y persists for a period and decays to zero as time passes by. There are in the literature many different models that deal with this kind of situation. This paper aims to review some of these proposals and show that under some fairly simple reparametrization they fall into a particular case of a class of Dynamic Linear Models (DLM), the transfer functions models. Inference is performed following the Bayesian paradigm. Samples from the joint posterior distribution of the unknown quantities of interest are easily obtained through the use of Markov chain Monte Carlo (MCMC) methods. The computation is simplified by the use of the software WinBugs. As an example, a consumption function is analysed using the Koyck transformation and the transfer function models. Then a comparison is made with classical cointegration techniques.