Abstract

Eigth Valencia International Meeting, Spain.

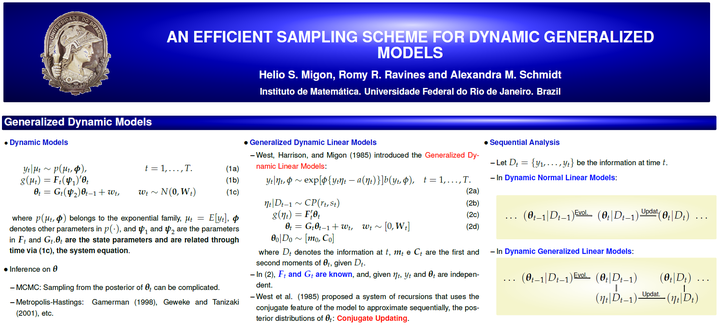

We consider non-linear state-space models for univariate time series with non-Gaussian observations in a Bayesian framework. For practitioners computational efficiency is always a desirable feature. We present a scheme for multimove sampling of the states parameters of such models within a Gibbs sampling algorithm. Our proposed sampling scheme combines the conjugate updating of West, Harrison, and Migon (1985) for dynamic models in the exponential family, with the Backward Sampling of Frühwirth-Schnater (1994).

We call this algorithm Conjugate Updating Backward Sampling (CUBS).

We notice that CUBS significantly reduces the computing time needed to attain convergence of the chains, being also simple to implement.

Samples from the posterior distribution of other parameters in the models can be obtained using standard MCMC techniques.

A quite extensive Monte Carlo study was conducted in order to compare the results obtained with CUBS with those obtained from some algorithms previously proposed in the Bayesian literature.

You don't have a PDF plugin, but you can download the PDF file.